Ring has done it again. The chart below shows the changes from Q4 2016 to Q1 2017 for the various DIY doorbell cameras. Ring, August and Skybell all saw happier users in the post Holiday installation frenzy. Skybell saw flat demand while August Home slipped and Ring had about a 5% increase in demand over Q4 2016.

Q1 2017 Snapshot of DIY Doorbell Camera Market Showing the Continued Dominance of Ring

Part of Ring’s leadership comes from their Installation experience. When we analyze the reviews of the top three brands, you can see all have frustrations with installation experience. Ring, by far, has the easiest installation, including their Initial Router Connection. Skybell and August both suffer from issues in Software Installation, initial Wiring and the included Instructions. If both brands focused a bit more on addressing these issues with installation, they could gain on Ring’s marketshare and grow their own revenues.

Comparison of Top Doorbell Camera Installation Experience As Rated By Consumers

This misses Do It For Me Doorbell Cameras like Vivint’s very popular model. Though we see people cite Vivint’s Doorbell Camera as a key deligher in their review of the app that controls their overall Vivint Smart Home experience. As Ring expands their ecosystem with the integration of Zonoff, we’ll see more direct competition between the DIY and DIFM leaders.

You can track that evolution in real time as it happens using the Argus Analyzer. You learn more as to how to access the evidence you need to snag your unfair share of the Smart Home Market using our leading tools.

One of the top articles being shared in the IoT Conversation is one on the improvements made to public transit in the very crowded but much loved Randstad area of the Netherlands. By leveraging a mix of infrared sensors, bluetooth and WiFI connectivity, the train system has been successful in monitoring and reacting to the travel patterns of consumers, improving flow and reducing crowding. It is a wonderful example of the shifts we are starting to see with the deployment of the Internet of Things or this case #internetOfWatchingHumansToImproveTransitFlow.

Many IoT applications look to mount sensors and radios on things that are in motion, something that drives increased battery life and minimal capabilities at the endpoint. This application in the Netherlands reverses this architecture brilliantly (because we have yet to chip the global population just yet) and now the trains come to us. Imagine the time shifting that can take place, knowing that when you arrive at the station for what used to be a harrowing commute into the local metropolis, a train will be mustered to meet your needs. This is a huge improvement over rigid schedules that force the population to converge on a single location in vain hopes of catching the same train into town.

If you’d like to get real time updates on when the IoT market pops, you can sign up for a free Argus Alerts subscription here. With over a million IoT tweets a month, the only way to stay on top of it all is using our platform to ensure your team is moving the market narrative in the direction of growth and influence.

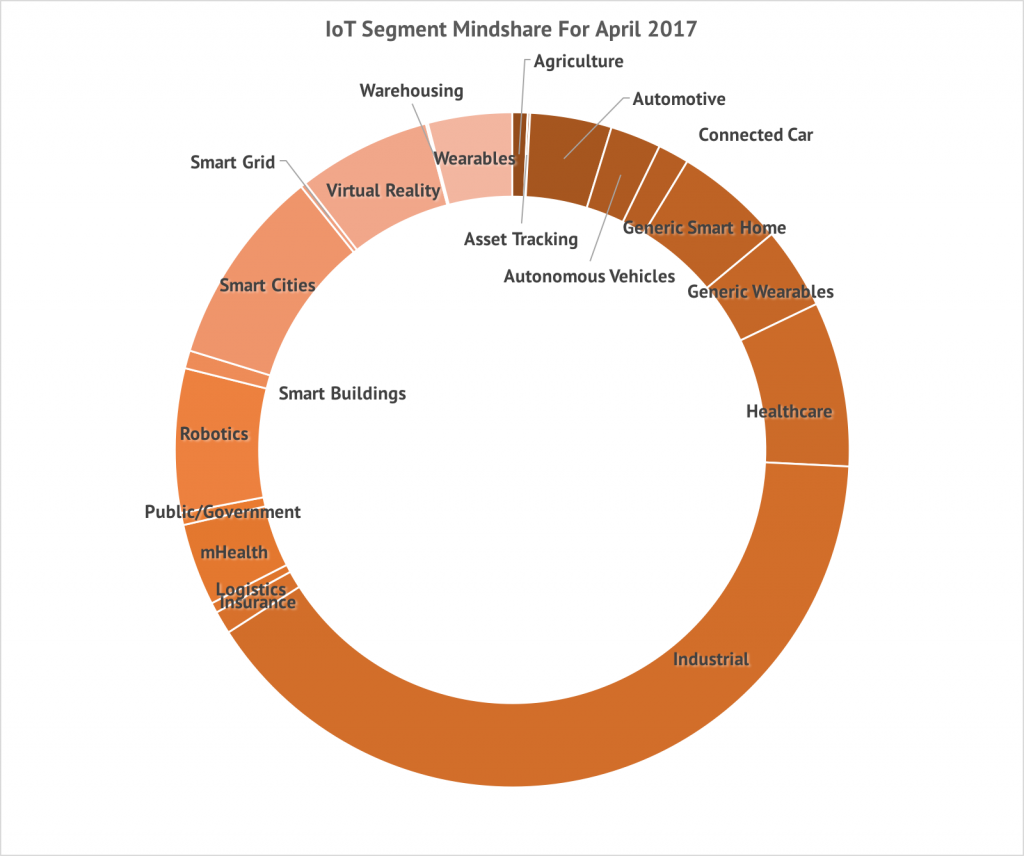

We are continuously gathering all of the Twitter traffic around IoT. It’s a dataset that goes back years! When you have ALL of the data, the ability to ask questions like “Which IoT Use Case is getting the most attention?” becomes a fascinatingly simple exercise. Answering this question is the beginning of understand what Use Cases are top of mind for the market, what language is being used to describe early IoT deployments, and whether YOUR particular Use Case is a blue ocean of possibilities or blood red ocean of ferocious competition… As you can see from the Mindshare chart below, Industrial IoT is the blood red ocean right now, but for good reason. The promise of cost savings, shifting from CapEx to OpEx, increased productivity and more mean that many of the early adopters of the potentially ill-named Internet of Things market are from big industry and manufacturing sectors.

Share of Voice Chart for Internet of Things Use Cases for April 2017 showing continued dominance of Industrial IoT based on an analysis of over 1 million IoT tweets in April 2017.

Other markets also get attention. Smart Home continues to be the main consumer entry point for the Internet of Things, and while most consumers do not show up at Best Buy asking for IoT products, much of the market conversation, especially from Europe equates Consumer IoT with Smart Home. Same is true with the stagnating market of Wearables, still occupying a significant part of the IoT Mindshare compared to government or Smart Buildings.

Virtual Reality and Automotive are an interesting mix of consumer and enterprise, both getting significant share of voice within the conversation. More public works segments like Smart Cities and Healthcare broadly get more attention than generic mentions government applications of IoT. Early home runs in IoT of Logistics and Asset Tracking seem not to grab as much attention, largely because these are being lumped into Industrial applications of IoT and do not drive as much eyeballs as their significant impact on operations would suggest.

Now imagine if you had the ability to dig deeper into each of these markets. Understand what topics and channels are driving the conversations around Smart Agriculture or mHealth, to see where you brand impacts the narrative or is ignored by others because your competition’s siren song of adoption is drowning out your message.

Well, you can. Argus Insights makes all of the data and the tools to discover the evidence you need to move markets to your ways of thinking available through our Argus Analyzer tools. If you’d like to get access to the same tools we use to fuel our analysis of the IoT market narrative, you can find out more here. With over a million IoT tweets a month, the only way to stay on top of it all is using our platform to ensure your team is moving the market narrative in the direction of growth and influence.

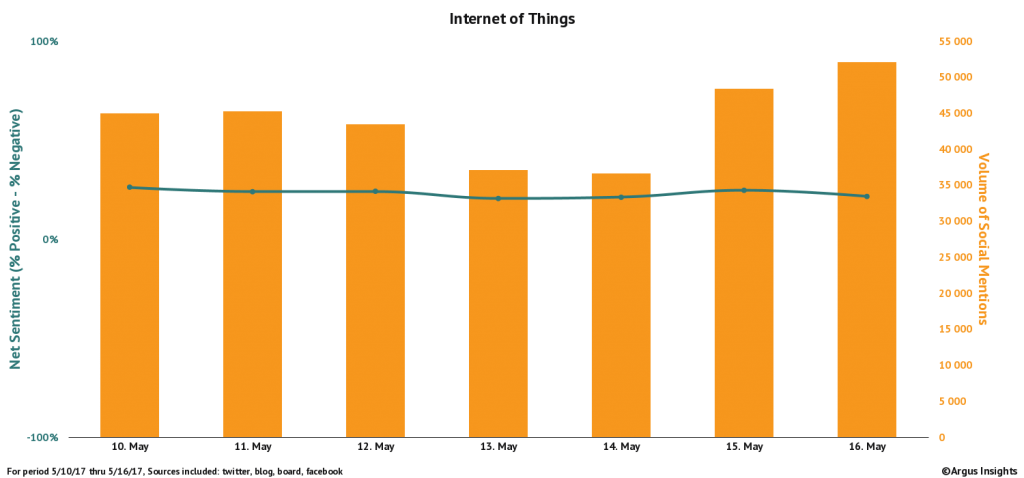

So this week, Silicon Valley is all abuzz with the IoT World event happening over at the Santa Clara Convention Center. Informa is touting at least 10,000 visitors. With a party that big, you’d think there would be ripple effects throughout the universe. Turns out not so much…

Little lift in IoT Tweets with the start of the IoT World Expo on 15 May 2017. Part of the lack of resonance might be the name…

Given how big the event was last year, what gives? Isn’t IoT going to be a huge market with over 50 billion endpoints in just a few years?!?! Probably, in fact our analysis shows that the number of deployments and POC’s taking place is accelerating over the past few months, sure signs of coming growth.

Question is, who is shopping? And what are they shopping for? Remember past B2B tech gold rushes? There is a big difference between how they were labeled compared to the Internet of Things. Think about Enterprise Resource Planning (ERP) or Marketing Automation or Customer Relationship Management (CRM). These are all named based on what they do for the customer, what need they satisfy. Use Hubspot to automate your marketing. Use SAP to provide better visibility of your resources and how they are being used. Subscribe to Salesforce to better manage those folks on the front lines of your customer relationships.

IoT doesn’t do that. It names a solution, not a need. It describes an architecture, a method, a platform, a pile of lego bricks waiting to be shaped by the creative genius of your organization. It does not speak in the language of the customers but in the language of the vendors. Prior incarnations fell into the same trap, Machine to Machine (M2M) describes the how, not the why. This labeling makes it even more difficult for customers looking for solutions to their needs to even see IoT as part of what could make them heroes in their organizations.

Imagine if you named Marketing Automation for it’s solution instead of it’s need. Hubspot would be a “multi-user collaborative SaaS application with predefined workflows in support of Marketing and Sales.” Salesforce would be sold as “distributed web application requiring no IT support designed as a database application that captures and reports on activities by sales teams.” Small wonder IoT has not caught on as fast we expect. It’s an issue of story telling and the power of names. CRM, ERP, and Marketing Automation were all industry names with the power to persuade, in the language of the customer’s needs, not the vendor’s solutions. The Internet of Things needs to shift into that same language to help vendors and buyers alike achieve the potential of these solutions, while calling it by a name that represents what the buyers need.

If you’d like to get access to the same tools we use to fuel our analysis of the IoT market narrative, you can find out more here. With over a million IoT tweets a month, the only way to stay on top of it all is using our platform to ensure your team is moving the market narrative in the direction of growth and influence.

I opened a Comtech Forum event on connecting the Internet of Things with this presentation. A couple of key pieces from the presentation I’ll spend a bit more time here describing.

The first is a meta analysis across multiple IoT device forecasts. While everyone has been bullish on IoT/M2M/whatever we are calling the market this month, when you look at the actual unit volumes published over the last few years, we are in that accelerating growth rate that marks an exponential. Taking it out further, we see significant growth by 2025 with an estimated 400 billion devices connected. This does not include the phones or wearables that other folks have ‘padded’ their forecasts with. The gut check I did was compare that number to the global population estimate for 2025, roughly 8 billion people. That means we could see 50 connected IoT devices for every person on the planet by 2025, not an unreasonable assessment given the number of IoT endpoints being used for industrial and municipal purposes.

The next slide I’d like to highlight is an analysis of the Trials, Deployments and Proof of Concepts (POC’s) being mentioned in Twitter. It’s increasing, at a substantial rate, month over month. All the while this increase is happening, the overall chatter has been relatively flat, meaning that more actual IoT work is getting done and talked about, reinforcing the belief that we are in an accelerating market, finally!

The last piece to mention is the slide on which protocols are being most referenced in the IoT Twitter chatter. As you can see from the chart, 5G dominates. But why? Unlicensed methods like Sigfox and LoRa are shipping in products today? LTE based licensed methods like Narrow Band IoT ( NB-IoT) or LTE Cat M1 are also seeing real deployments this year? Why all this hype around a licensed method that is barely off the workbench of the vendors?

Part of the hype is the 5G ecosystem working hard to accelerate adoption of the next generation even as service providers still have not squeezed the last bit of performance out of their LTE investment. Though keeping true to my view that it is really the Internets of Things, not a single network, there are many, albeit long tail, applications where 5G does not make sense. Applications that do not require the low latency and high bandwidth that 5G offers such as smart agriculture deploys in rural environments where low power and long range trump what 5G trumpets.

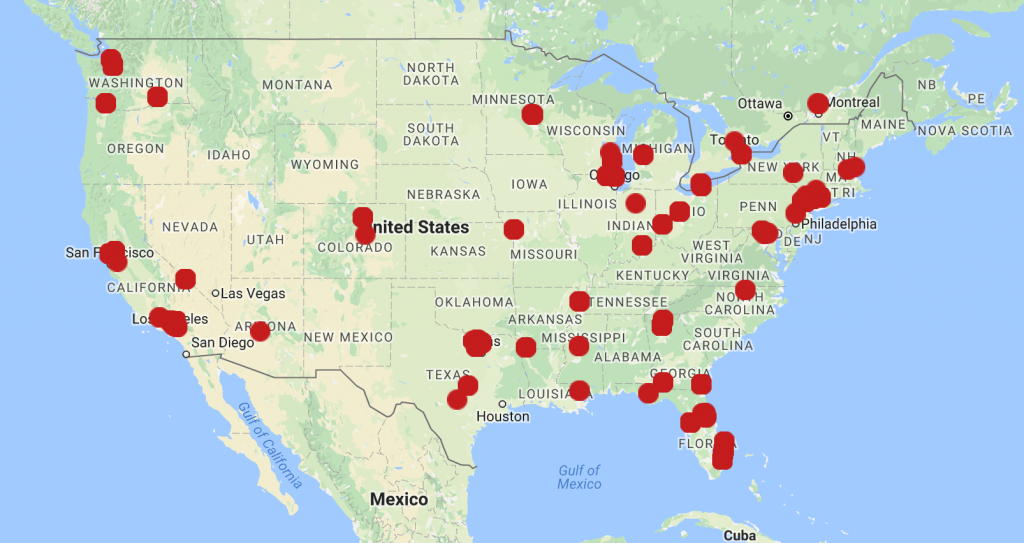

Two Weeks of Geolocated Tweets Mentioning IoT. Where there are not tweets are actually some of the regions where IoT will be transformative but probably not using 5G.

When we dig into the conversations around 5G, much is on trials happening with carriers. More than a few tweets question the readiness of IoT, pointing to the maturity of 5G as a reason IoT is not ready, even equating it to the Skynet of Terminator fame. What is also interesting is how conflated IoT and 5G are becoming. As a community we need to be clearer on where and how these protocols are valuable. At the Comtech Forum meeting, the overwhelming interest from the audience during our Unpanel was not on the protocols themselves but what markets they are/will impact. At the end of the day, the success of IoT will be measured by the rate the “how” (5G, LoRa, NB-IoT) disappears from from the conversation and we focus on the ‘what’ of Smart Cities, Smart Agriculture, Asset Management and hundreds of other applications we have yet to prove out for IoT.

If you’d like to get access to the same tools we use to fuel our analysis of the IoT market narrative, you can find out more here. With over a million IoT tweets a month, the only way to stay on top of it all is using our platform to ensure your team is moving the market narrative in the direction of growth and influence.

One of the top articles being shared in the IoT Conversation is one on the improvements made to

One of the top articles being shared in the IoT Conversation is one on the improvements made to