I am the founder and CEO of Argus Insights, a leader in Experience Analytics. Argus was started in stealth mode in 2008 to answer the question, "How can Market Research be improved and help drive innovation instead of validation?"I was the Executive Director of the ME310 Global Design Innovation Course at Stanford University. The course has a forty year history of developing tomorrow’s innovation leaders.Formerly I was the Chief Technologist for SK Telecom America’s R&D Group. In this role I was responsible for understanding how the rapidly changing technology landscape would enable SK Telecom to craft new business opportunities in the Americas. My areas of responsibility ranged from NGN wireless technologies (LTE vs WiMaxx, etc), handheld experiences & the interface technologies that enable them (multitouch touchscreens, haptic feedback, smartphone operating systems), as well as evolving influences on the telecommunications market (cloud computing, femtocells, CDN’s, LBS, SNS, etc.) I also supported SKTA’s internal Business Development & Corporate Venture Capital organizations.Prior to my role at SKTA, I led Synaptics efforts for developing next generation capabilities for handheld devices from within the marketing organization. I was responsible for developing a comprehensive competitive landscape for the various handheld markets, with specific focus on the mobile ecosystem, driving the product & technology strategy, in partnership with the engineering organization, to architect & execute our roadmap of future capabilities.I was also the architect of the Onyx Concept Phone, the world’s first multitouch mobile experience. I worked with the top handset manufacturers on the creation of tomorrow’s handsets, ensuring the right marriage of technology & user experience takes place as we see an industry transformation take place around multitouch technologies.

Strategy Analytics recently released findings that Android sales have been much higher than iPad sales. We’ve seen the iPad stumbling since the launch of the Gen 4 iPad and the iPad mini in the fall. The closing experience gap between Android and iOS tablets has led to eroding demand and aggressive price cutting by US retailers Walmart and Best Buy for new iPads to drive up sales. The only ace Apple may have up their sleeve for Q3 2013 is the rush by parents to equip students with tablets. Apple’s bet on retaking the education market by partnering with textbook publishers could pay out this fall as an increasing number of institutions require iPads for classroom use.

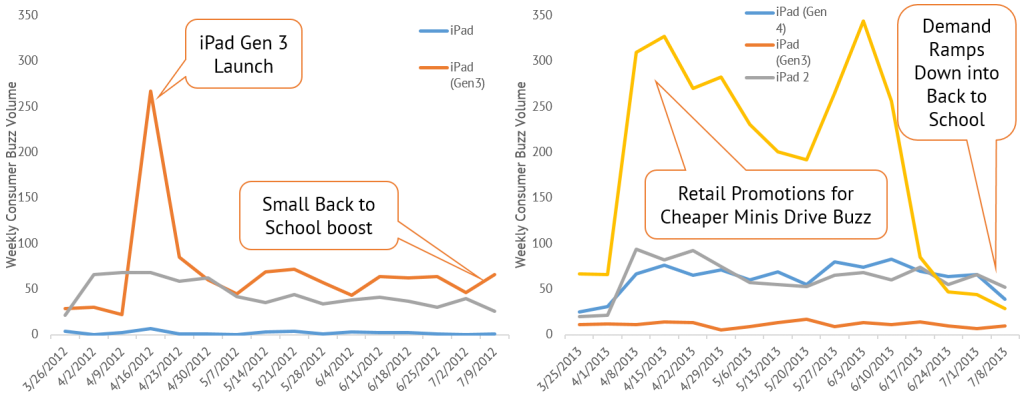

Comparing Back to School iPad demand for 2012 and 2013 shows demand sliding for 2013.

Issue is that we are seeing sliding demand as we head into Back To School season. After a spring of iPad mini promotions we are seeing saturation effects across all the iPads with the exception of older iPad 2 models still being snapped up. The impact on mini demand by a small price drop shows a saturation of iPad with newer experiences not requiring the same upgrade path that the iPhone has over the years. We think Strategy Analytics is on the right path with Q3 being another week iPad quarter. If we see things change, we will let you know!

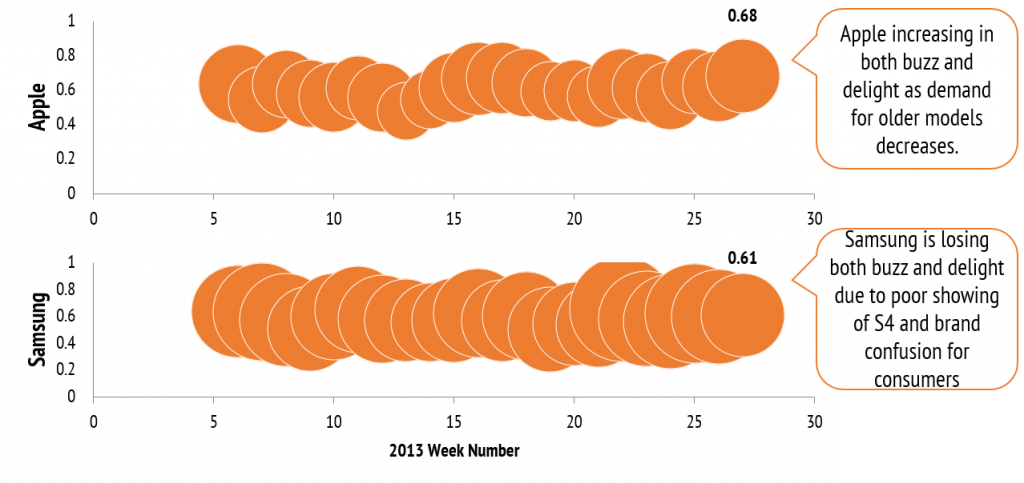

As Samsung reports their quarterly report with a mix of excitement and caution (Samsung Boosts Capital Spending as High-End Phone Demand Slows – Bloomberg), Argus Insights sees their caution warranted for Q3. July brought the first significant drop in consumer buzz for Samsung Smartphone in a long time. What made the drop even more poignant was that Apple saw a boost in demand. This drop in buzz was coupled with a drop in delight meaning that consumers expectations for what a Samsung Smartphone brings to their lives are not being met.

Samsung is starting to slide against Apple in the hearts and minds of consumers. This portends a lackluster Q3 for Samsung.

The weakness of the S4 coupled with the desire to phase out the S3, compounded by the confusing launch of four separate Galaxy Note 3 handsets this fall portends a challenging 2013 for Samsung. The market leader has to lead the market in more than just sales and invention of technology driven features, it has to lead with value and innovation to the end user.

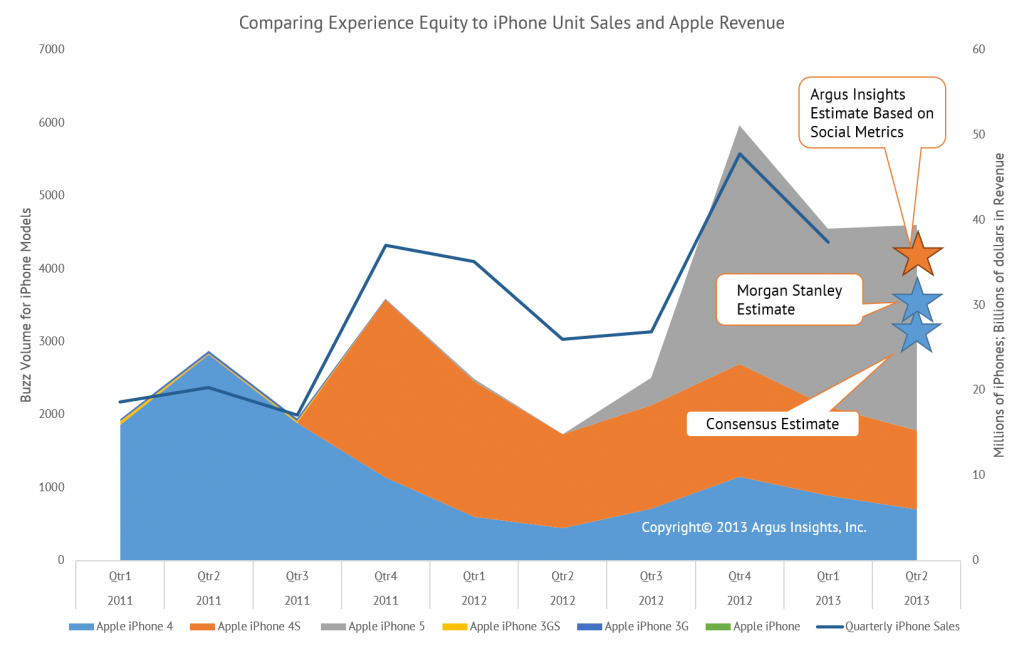

CNet reports that Morgan Stanley Analyst, Katy Huberty says iPhone shipments will hit at least 29 million last quarter. Our analysis based on our social media power metrics of consumer demand say that Katy is being more conservative than the market realizes. Our quarter to quarter analysis of consumer demand through our Experience Equity metrics show a surge in demand last quarter for iPhones, especially the iPhone 5. We saw the first major drop in demand for the iPhone 4 and iPhone 4S handsets as price conscious consumers got their deal fix. iPhone 5 demand was buoyed by one of the most aggressive ad campaigns we’ve seen from Apple to date judging by the promotion emails even to our recruiting email at Argus Insights.

Apple has also been helped by retail partners getting creative with iPhone 5 specials such as Best Buy’s well received iPhone trade-in promotion in which qualified consumers could walk out with a brand new iPhone 5 for the cost of sales tax. The iPhone 5 was also helped by the lackluster launch of the Galaxy S4, which many consumers waited to see if it would compete with the iPhone. We see the results of the aggressive promotions, Samsung snafus and resulting increase in purchasing behavior in the proprietary way we track consumer demand.

Based on proprietary consumer demand metrics of social capital, Argus Insights suggests that Apple’s Q2 iPhone shipments will be significantly higher than the consensus estimate of 26.2 million.

So what’s our guess? Based on the rough analysis we’ve done, iPhone sales will be north of 30 million (as high as mid 30’s to be honest) and more iPhone 5’s than in the past, giving a corresponding boost to both revenue and earnings for Apple in Q2 (fiscal Q3). As a result, Wall Street should be pretty delighted by what Apple feeds them during the earnings call.

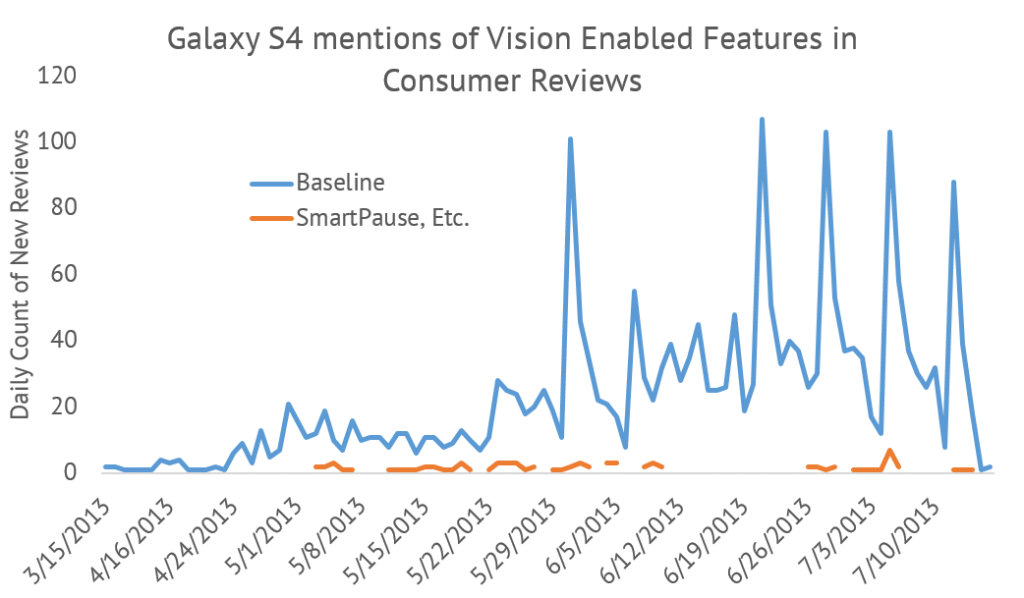

We recently did some analysis for the Embedded Vision Alliance looking at consumer adoption vision technologies in consumer electronics. If you’re curious, you can see the slides here. The shocking result was how little of the Galaxy S4 customers even mention the eye-tracking features. The graph below shows the volume of eye-tracking mentions compared to the overall mentions. Previously we’ve commented on the S4’s poor launch into the market but this may shed some light as to why that’s was the case.

Galaxy S4 Consumer barely mention the novel eye-tracking features, and typically negatively.

Samsung’s biggest push in the marketing was the ability of the Galaxy S4 to do cool things by tracking your eyes. It was featured in all their commercials and was the backbone of their “next big thing is already here” campaign refresh. Turns out it wasn’t that important to consumers. Less than 5% even mentioned what Samsung considered to be the most important feature of the Galaxy. Let’s put a fine point on that. Samsung spent millions of dollars telling the world about these vision based interface features and it only resonated enough with 5% of their customers to even mention it?

Here’s the kicker, of that 5%, over 60% did not like the feature. They found it “twitchy” or “erratic”. One particularly passionate consumer even called it “fake.” The other theme that arose from the naysayers was the impact these features had on battery life, causing their S4 to lose joules faster than Coca Cola’s share price evaporating.

To be fair, those that loved these features, really loved them and found Samsung’s brand promise of a “Life Companion” rings true. But that was for just 2% of all consumers that bothered to review the product.

This could be the reason the S4 was slow the launch. The features that Samsung pushed in an effort to drive demand literally no one wanted. When you strip the vision features from the S4, it looks a lot like the S3 (which is still doing brisk sales by the way). Like selling solar powered heaters in the Sahara, Samsung staked their flagship launch on what the market did not want. Pushing features over experience will do that to you. While the Galaxy S4 seems to be recovering now, its not that more consumers are discussing Smart Pause. Consumers cite the screen size, application responsiveness, anything but the vision based features, as reasons for purchase. LG just released a firmware update to enable the same feature set on the LG Optimus G Pro and so far no one has even mentioned it. The market is not yet ready, partly for performance issues, partly for not finding compelling needs that these features solve for. Maybe the S5…

Sprint has finally been taken off the market by Softbank. In addition to a reasonable spectrum footprint in the United States, good relationships with M2M players like Amazon (Kindles get books delivered through Sprint), regional advantages in the midwest, and the largest population of grumpy customers in the United States. Grumpy? Since when could we measure grumpiness? In our weekly reporting of shifts in Smartphone consumer demand, we analyze the different consumer handset engagements by major carrier. Since we started doing the analysis, we noticed that Sprint customers, for the same handsets, were more disappointed than their peers from other carriers.

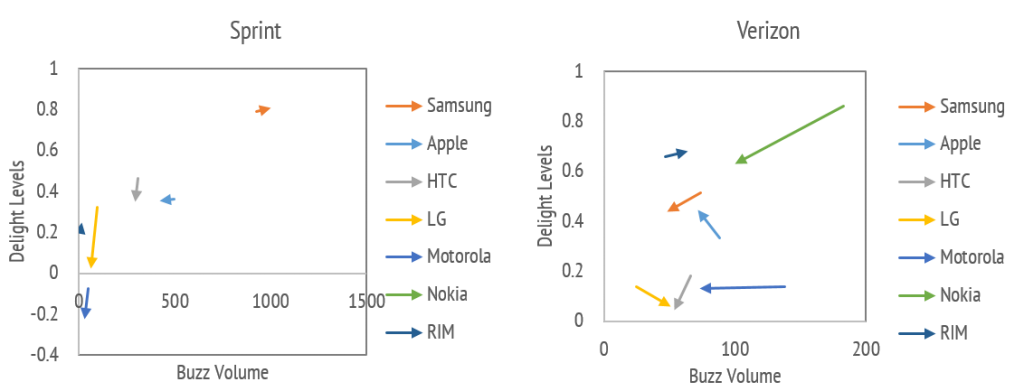

Comparison of Handset OEM brand perceptions between Sprint and Verizon. With the exception of Samsung, all brands at Sprint are disappointing consumers.

The chart above shows a month to month comparison in the overall OEM perception trends for Sprint and Verizon. Of all the carriers we track, Sprint has the lowest Delight levels. Verizon customers are, on average, twice as delighted as Sprint customers. Thank goodness Sprint is carrying Samsung handsets, which are responsible for the only population of happy customers at Sprint.

For Softbank, the opportunity is to understand what about the Sprint experience is driving such melancholy and reinforce the strong ties with Samsung. Apple is a distant second to Samsung at Sprint, signaling continued erosion of Apple’s mindshare in the United States.

If you are interesting in unpacking specific differences between Sprint and other carriers or what about Samsung’s handsets seem to be delighting Sprint consumers, let us know. We are now publishing our weekly Peek™ report for Smartphones that provides where the shifts in consumer demand are going. Subscribe here.