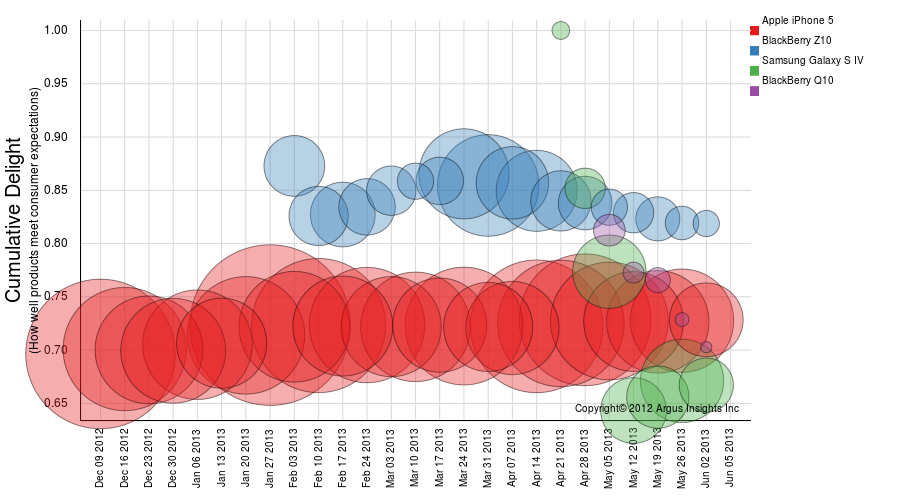

While the Q10 is finally coming to America, it is unlikely to do as well as the Z10 has in the battle for hearts and minds. We’ve been tracking the Q10 in Canada and the UK since it was released weeks ago. The initial response has been poor, both in terms of buzz and delight, especially when compared to the triumphant release of the Z10.

Notice that the Z10 is slowing but still perceived by consumers as a better experience than even the iPhone 5. We’ll see if Monday’s Apple event shifts that perception. The Q10 is barely demanding commentary from the early markets, signally a slow start as it comes to the United States this week. Maybe the days of physical keyboards on phones have finally passed us by? We will have a surprise on Monday for Apple’s event so stay tuned!

When the iPad Mini was launched in late 2012 it was into an already confused consumer market of the Apple faithful. The iPhone 5 had been launched weeks earlier to a largely yawn response from the market (though it’s improving now). The iPad 4 launched with the Mini, and out of the normal cycle consumers had come to expect from Apple, largely delivered what consumers expected from the iPad 3 in March of 2012. Along with the release of the iPhone, Apple released new iPod Touch, known commonly the gateway drug to full iPhone ownership, but at a reasonably high price point. This put Apple in a pricing squeeze play for the Mini, pricing it twice as much as it’s comparable competitors. As a result we saw slow adoption for the iPad Mini and even the iPad 4 around the holiday season.

Cut to today and we see demand spiking in a way we have not seen for an Apple product since the iPhone became available on Verizon. In wallowing through the social media analysis, we found the culprit. Apple allowed retailers to drop the price by a significant percentage in April, ahead of Mother’s Day and after probably having a disappointing Valentine’s Day. This is typically unheard of for Apple to allow a price drop before launching another product. The punchline? Apple is losing its ability to demand a premium from the market. A smaller iPad is cool but not enough to compete against the much cheaper but almost equivalent experience of the Kindle Fire. Apple will have to pull more than one rabbit from their hat at the event on 10 June. Argus Insights is preparing a special surprise to assess the market impact of Apple’s announcements. More soon!

There’s a problem in social media analytics today. Spam. Spam in more flavors and varieties than even Hormel has produced to satisfy the crazed cravings of the market. The first type of spam we see is classic ecommerce ads. Acer Laptop replacement batteries, iPhone 4 cases, Kindle Fire starter, you name it. We did a brand audit of Best Buy in August 2012 and found that over 30% of all Best Buy mentions contained links to Amazon.com.

Right before the holidays, Facebook users became party to one of the single largest ecommerce spam campaigns we’ve seen in our customer work. Amazon Affiliate Bob Douplein, or an agent acting on his behalf, found a way to post the entire Amazon.com product catalogue on millions of public Facebook profiles, over 14.4 million according to Google. This had a huge impact on accurately tracking brand perception by users for our customers for such obvious spam, but Bob’s Page Rank improved. Tactics like this emerge faster than Facebook or Twitter can respond which means bad data leaks into everyone’s social streams. This is part of the reason we don’t charge our customers per mention like the other guys but instead go for broad terms and help narrow to what’s really consumers and what’s not.

Social Media offers more varieties of Spam than even Hormel!

The second type of spam we’re seeing more and more are Twitter Bots and the family tree for this branch of spam is getting more and more diverse as the bot makers get more creative. The first bots we were seeing were retweet bots, types that searched the twittersphere for content related to either keywords or specific authors and then just blindly retweet. The number of @engadget, @verge, @mashable retweet bots just boggles the mind. Some articles are legitimately retweeted by actual humans that like the piece and want to share it out but more are bot driven. These bots are mostly benign and help drive awareness for mostly interesting content.

A second type of twitter bot we’ve seen are those masquerading as real people. They typically have few followers but somehow manage to tweet every 5-15 seconds, and in multiple languages! Sure I might speak English, a bit of Japanese and my native Arkansan but these are twitter users that routinely tweet in Indonesian, Japanese, Arabic, Portuguese, English and French on the same day! What’s even more insidious about these tweets is that they are shared across a network of bots which means the individual tweets are copied across multiple accounts in pseudo random ways to spread the message broader. I could go on but I’ll wait for another post to do so. The third act is what we’re doing about the spam in social media. We’re slowly building our arsenal of spam detectors to separate the wheat from the chaff, and ensuring our clients have the purest feeds of their consumers to base their decisions. What type of spam have you been fighting in social? Together we can make social media represent the true Voice of Market rather than a precursor to SkyNet.

We’ve checked our math over twenty times, gone back to the sources to verify what we’re seeing in the data from the market, but there’s no other conclusion we can draw, the Galaxy S4 is having what can only be termed a terrible launch. What? How can we say that? The S3 was the biggest threat to the iPhone 5 since the iPhone 4S! See it for yourself, the demand for S4 is much slower than the same time frame as its competitors.

Samsung Galaxy S4 Wilts During Spring Launch

Samsung has fallen into the same trap as Apple where the only thing consumers wanted more than a new iPhone 5 was a cheaper iPhone 4S. The same logic seems to playing itself out for the Galaxy S4, with a surge in response to both the S3 and iPhone 5.

Samsung Galaxy S4 Now Ranked Below iPhone 5

We saw the market demand pause when the S4 was announced back in market (you can see the iPhone 5 bubble shrink a bit) but as soon as the S4 was available, iPhone 5 surged. Part of this is challenges in continuous innovating the user experience (eye tracking is like Siri, novel at first taste but annoying after), partly due to Apple getting aggressive with iPhone 5 promotions, rolling up their sleeves and wading into the brand wars everyone else is fighting. The smartphone market is insanely dynamic. Waiting for quarterly reports means you miss the chance to take advantage of these changes. That’s why Argus Insights tracks the market continuously. Look for our soon to be released weekly consumer demand report.

Beware the Ides of March said the soothsayer to Julius Caesar before he was brutally murdered by his customers. With the launch of the Galaxy S IV, the same could have been said for Samsung. The fanfare around the launch was new for Samsung, seeking to gather as many eyeballs as Apple does for their cryptic events. While tech pundits complained about the mash-up betweenMad Men and Leave it to Beaver (rightfully so it seems), Argus Insights was busy understanding how the big S compared to the big A with their Big Apple (pardon the pun) event.

When we compared the hourly social mention volume between the iPhone 5 launch in September 2012 and the March 14, 2013 launch of the Samsung Galaxy S IV, there is no comparison. The iPhone 5 event attracted almost 10X the buzz of Samsung. Samsung did beat out RIM’s BB10 launch in January by a fair margin, almost 2X.

So little surprise that Samsung wasn’t able to compete with the iPhone 5 launch. The silver lining is that Samsung didn’t have the post launch fall off that Apple or RIM did.

When we normalize for the days prior the launch, though Samsung comes in third place, meaning that both Apple and RIM had bigger lifts in social media in comparison. While the RIM overall volume may have been the lowest, it was a big event for them, pushing proportionally more awareness than the Samsung event.

How will this translate to sales of the Galaxy S IV? Reach out to Argus Insights to find out. We’ll be releasing our new Smartphone and Tablet Demand Side Forecast in the middle of Q2. Email if you’d like a free copy of the inaugural issue, sales@argusinsights.com.