Strategy Analytics recently released findings that Android sales have been much higher than iPad sales. We’ve seen the iPad stumbling since the launch of the Gen 4 iPad and the iPad mini in the fall. The closing experience gap between Android and iOS tablets has led to eroding demand and aggressive price cutting by US retailers Walmart and Best Buy for new iPads to drive up sales. The only ace Apple may have up their sleeve for Q3 2013 is the rush by parents to equip students with tablets. Apple’s bet on retaking the education market by partnering with textbook publishers could pay out this fall as an increasing number of institutions require iPads for classroom use.

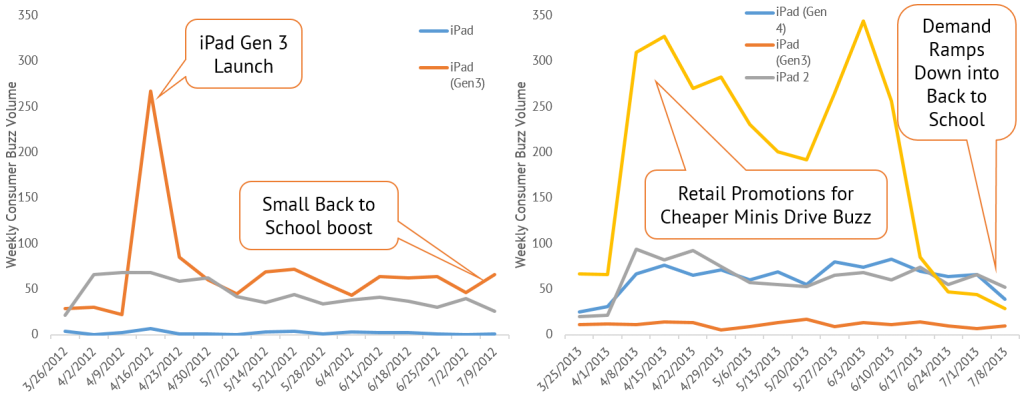

Comparing Back to School iPad demand for 2012 and 2013 shows demand sliding for 2013.

Issue is that we are seeing sliding demand as we head into Back To School season. After a spring of iPad mini promotions we are seeing saturation effects across all the iPads with the exception of older iPad 2 models still being snapped up. The impact on mini demand by a small price drop shows a saturation of iPad with newer experiences not requiring the same upgrade path that the iPhone has over the years. We think Strategy Analytics is on the right path with Q3 being another week iPad quarter. If we see things change, we will let you know!

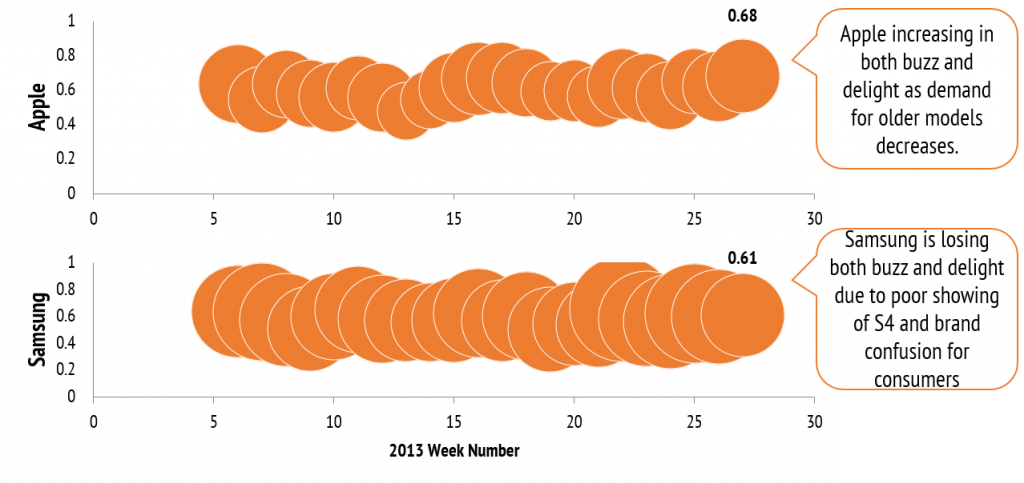

As Samsung reports their quarterly report with a mix of excitement and caution (Samsung Boosts Capital Spending as High-End Phone Demand Slows – Bloomberg), Argus Insights sees their caution warranted for Q3. July brought the first significant drop in consumer buzz for Samsung Smartphone in a long time. What made the drop even more poignant was that Apple saw a boost in demand. This drop in buzz was coupled with a drop in delight meaning that consumers expectations for what a Samsung Smartphone brings to their lives are not being met.

Samsung is starting to slide against Apple in the hearts and minds of consumers. This portends a lackluster Q3 for Samsung.

The weakness of the S4 coupled with the desire to phase out the S3, compounded by the confusing launch of four separate Galaxy Note 3 handsets this fall portends a challenging 2013 for Samsung. The market leader has to lead the market in more than just sales and invention of technology driven features, it has to lead with value and innovation to the end user.

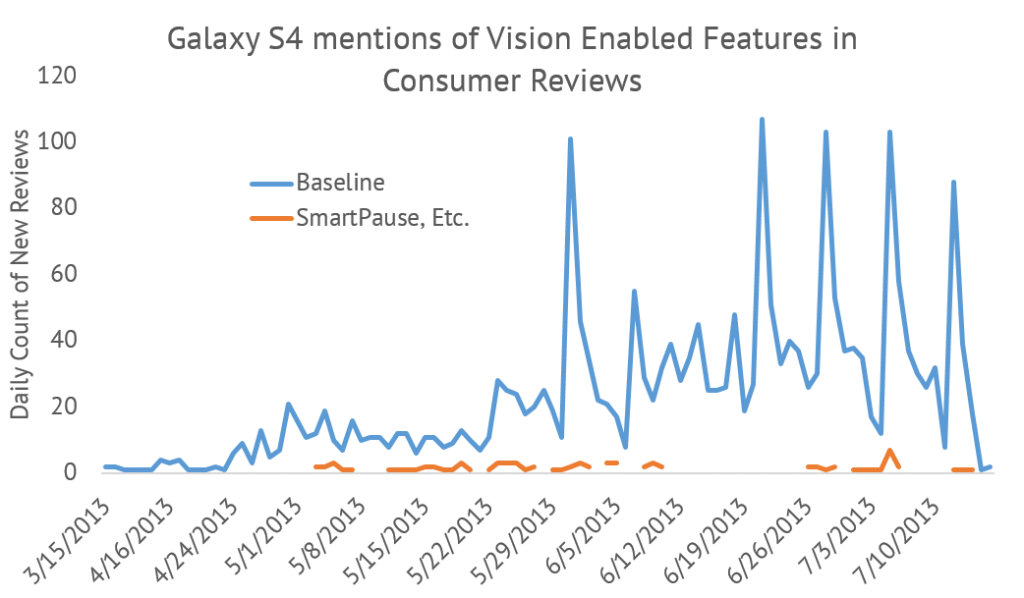

We recently did some analysis for the Embedded Vision Alliance looking at consumer adoption vision technologies in consumer electronics. If you’re curious, you can see the slides here. The shocking result was how little of the Galaxy S4 customers even mention the eye-tracking features. The graph below shows the volume of eye-tracking mentions compared to the overall mentions. Previously we’ve commented on the S4’s poor launch into the market but this may shed some light as to why that’s was the case.

Galaxy S4 Consumer barely mention the novel eye-tracking features, and typically negatively.

Samsung’s biggest push in the marketing was the ability of the Galaxy S4 to do cool things by tracking your eyes. It was featured in all their commercials and was the backbone of their “next big thing is already here” campaign refresh. Turns out it wasn’t that important to consumers. Less than 5% even mentioned what Samsung considered to be the most important feature of the Galaxy. Let’s put a fine point on that. Samsung spent millions of dollars telling the world about these vision based interface features and it only resonated enough with 5% of their customers to even mention it?

Here’s the kicker, of that 5%, over 60% did not like the feature. They found it “twitchy” or “erratic”. One particularly passionate consumer even called it “fake.” The other theme that arose from the naysayers was the impact these features had on battery life, causing their S4 to lose joules faster than Coca Cola’s share price evaporating.

To be fair, those that loved these features, really loved them and found Samsung’s brand promise of a “Life Companion” rings true. But that was for just 2% of all consumers that bothered to review the product.

This could be the reason the S4 was slow the launch. The features that Samsung pushed in an effort to drive demand literally no one wanted. When you strip the vision features from the S4, it looks a lot like the S3 (which is still doing brisk sales by the way). Like selling solar powered heaters in the Sahara, Samsung staked their flagship launch on what the market did not want. Pushing features over experience will do that to you. While the Galaxy S4 seems to be recovering now, its not that more consumers are discussing Smart Pause. Consumers cite the screen size, application responsiveness, anything but the vision based features, as reasons for purchase. LG just released a firmware update to enable the same feature set on the LG Optimus G Pro and so far no one has even mentioned it. The market is not yet ready, partly for performance issues, partly for not finding compelling needs that these features solve for. Maybe the S5…

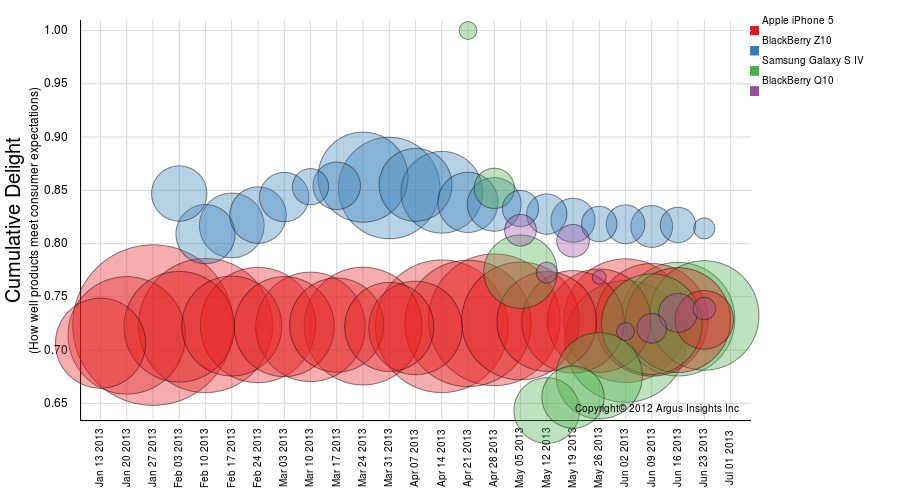

For the company formerly known as RIM, Friday was a tough day because of revelations that fewer than half of the handsets sold were BB10 handsets according to BlackBerry pleads for patience after brutal quarter | Mobile – CNET News. While CNet puts blame on the launch of the Q10 after the Z10, our analysis finds that the issue isn’t the launch order of the new products but consumer concerns with the Q10 in specific.

Slowing demand for Z10 and initially poor consumer response to Q10 drive slow sales of BB10 devices for BlackBerry’s most recent quarter.

As you can see in the comparisons to the Apple iPhone 5 and the Samsung Galaxy S4, BlackBerry’s new handsets are experiencing slack demand. The initial delight around the Z10 has stabilized above the iPhone 5, showing that the early adopters of BB10 are delighted by the innovations embedded in the interface. The Q10, by contrast, has had a rougher start with few consumers even bothering to share their views, a key indicator of poor demand though recently it has gained in both delight and buzz. Overall, our results tell the story that the market is viewing BlackBerry as two companies, the stalwart producer of email focused, QWERTY enabled handsets and an upstart entrant into the smartphone market that has to play by the same rules of any new brand entering a market. The issue is the upstart has not yet sparked the frenzy BlackBerry or Wall Street needs or expects.

We will be digging into the differences in user expectations for the Q10 and the Z10 in this week’s Smartphone Consumer Demand Report. You can sign up to receive the report here and get weekly updates on what is driving Smartphones while your competition is still waiting for their quarterly report to download…

The street is all a twitter regarding Samsung Galaxy S4 sales estimate: 30% below expectations | BGR. We called this weeks ago with our coverage of the S4 launch. Turns out our analysis was spot on, that the S4 wasn’t having the same demand as the hype would suggest. This points out the fallacy of most forecasting methods based on sell-in rather than consumer demand metrics similar what we have developed at Argus Insights. Our analysis shows consumer dissent around a laggy performance and battery challenges with both life and charging. All the “features” added in the Galaxy S4 have clogged the experience for consumers and provide evidence that Samsung is still learning how to provide an integrated user experience rather a series of features chained together by marketing ads.